Introduction: You’re Not Bad With Money — You Just Need a Plan

Does looking at your bank account make your stomach drop? Do you have multiple debts spread across credit cards, student loans, or car payments — and no clear idea of where to even start?

You’re not alone. Millions of people feel paralyzed by debt, not because they lack willpower, but because they lack a system.

That’s exactly why a debt payoff planner printable can be a game-changer.

Instead of keeping your debt in your head (where it feels 10x scarier), you put it on paper — organized, prioritized, and trackable. One page. Total clarity. And a plan you can actually follow.

In this guide, you’ll learn the two most powerful debt payoff methods, how to use a debt payoff planner printable to execute either one, and where to grab a free template today.

Let’s get you on the road to debt freedom.

What Is a Debt Payoff Planner Printable?

A debt payoff planner printable is a structured worksheet — printed or digital — that helps you list all your debts, organize them by priority, track your monthly payments, and visualize your path to being debt-free.

Think of it as a GPS for your finances. Without it, you’re driving blind. With it, you know exactly how far you’ve come and how far you have left to go.

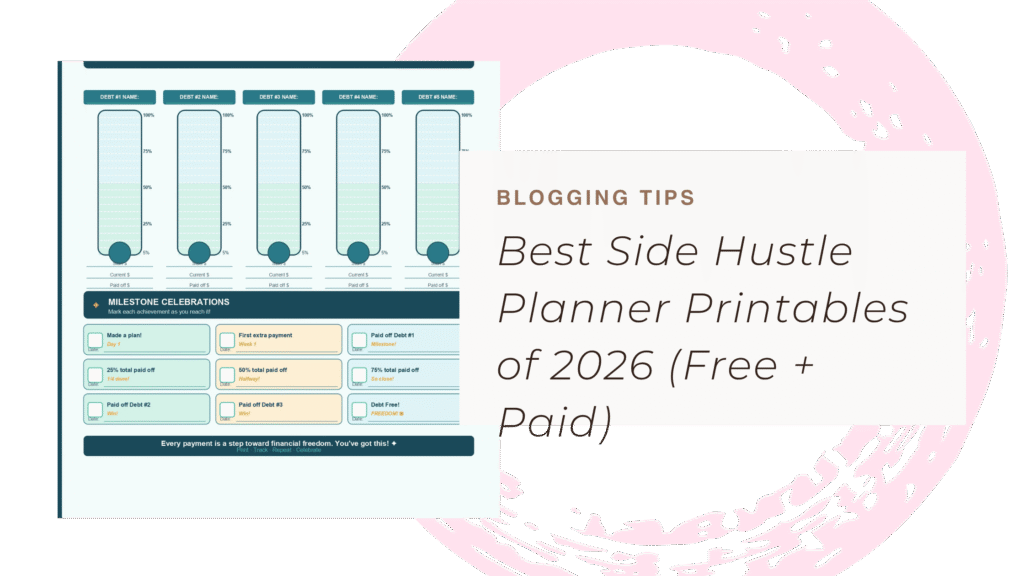

A quality debt tracker template typically includes:

- A space to list all your debts (creditor name, balance, interest rate, minimum payment)

- A monthly payment tracker

- A running balance calculator

- A progress bar or visual milestone tracker

- Space for notes or motivational checkpoints

When paired with a budget planner printable, it becomes a complete financial management system you can use every single month.

5 Reasons a Debt Payoff Planner Printable Actually Works

You’ve probably tried willpower alone. Here’s why adding a printable planner changes everything:

1. It makes the invisible visible. Debt lives in your head as a vague, looming cloud of stress. Writing it down on a debt tracker template turns it into concrete, manageable numbers. Numbers you can work with.

2. It gives you a clear priority order. Knowing which debt to attack first removes the paralysis of not knowing where to start. No more paying random amounts to random accounts.

3. It builds unstoppable momentum. Crossing off a paid debt — even a small one — releases dopamine. Progress feels good, and that feeling keeps you going.

4. It keeps you accountable every month. Your debt payoff planner printable becomes a monthly ritual. You sit down, update your numbers, and remind yourself of the mission. That consistency compounds over time.

5. It shortens your payoff timeline. People who track their debt pay it off faster — not because the math changes, but because awareness prevents backsliding and encourages extra payments.

Debt Snowball vs. Debt Avalanche: Which Strategy Is Right for You?

Before you fill in your debt avalanche worksheet or debt snowball tracker printable, you need to pick a strategy. Here’s a clear breakdown of both:

The Debt Snowball Method

How it works: Pay off your smallest debt first, regardless of interest rate. Once that’s gone, roll that payment into the next smallest debt. And so on.

Best for: People who need quick wins to stay motivated. If you have a $300 credit card balance you can knock out in 2 months, that win will fuel your next 6 months.

The psychological edge: Momentum. The snowball method is less mathematically optimal, but research shows it works better for most people because of the emotional boost from eliminating accounts quickly.

Use a: Debt Snowball Tracker Printable — organized from smallest to largest balance.

The Debt Avalanche Method

How it works: Pay off your highest-interest debt first. Once it’s eliminated, move that payment to the next highest rate.

Best for: People who are analytically motivated and want to minimize total interest paid over time.

The financial edge: You’ll pay less overall. If you have a high-interest credit card at 24% APR, every extra dollar you throw at it saves you money that the snowball method can’t.

Use a: Debt Avalanche Worksheet — organized from highest to lowest interest rate.

Not sure which to choose?

Use the snowball if you’re struggling to stay motivated or have several small debts. Use the avalanche if you’re disciplined and want to pay the least amount of interest possible.

Either way, a debt payoff planner printable makes both strategies easy to execute.

How to Use a Debt Payoff Planner Printable: Step-by-Step

Here’s exactly how to get started today:

Step 1: List Every Debt You Have Don’t skip anything. Write down every credit card, loan, and “buy now, pay later” balance. Include the creditor name, current balance, interest rate, and minimum monthly payment.

Step 2: Choose Your Strategy Snowball (smallest balance first) or Avalanche (highest interest first). Pick one and commit to it.

Step 3: Order Your Debts Accordingly Reorder your list based on your chosen method. Your #1 debt is the one getting all your extra money each month.

Step 4: Set Your Monthly Budget Use a budget planner printable alongside your debt planner to identify how much extra money you can direct toward debt each month — even $25 extra makes a difference.

Step 5: Make Your Minimum Payments on Everything Else Never miss a minimum payment on any account. All extra money goes to debt #1 only.

Step 6: Update Your Tracker Every Month Log each payment, update your balances, and watch your progress grow. This step is non-negotiable. The tracker only works if you use it.

Step 7: Celebrate Milestones When you eliminate a debt, celebrate (affordably!). Then immediately redirect that payment toward your next target.

Download Your Free Debt Payoff Planner Printable

Ready to stop stressing and start making real progress?

👉 Download Your Free Debt Payoff Planner Printable at GuidedPlanners.com

Our printable bundle includes:

✅ A Debt Snowball Tracker Printable

✅ A Debt Avalanche Worksheet

✅ A Monthly Budget Planner Printable

✅ A Debt Overview Tracker Template

✅ Progress milestone checkpoints to keep you motivated

No complicated apps. No subscriptions. Just print, fill in, and get started.

Start your debt-free journey today — download is instant and completely free.

7 Tips to Stay Consistent and Pay Off Debt Faster

Having the right debt payoff planner printable is step one. Staying consistent is step two. Here’s how:

- Schedule a monthly “money date.” Sit down on the same day each month to update your tracker. Put it in your calendar like an appointment.

- Automate your minimum payments. Remove the risk of missed payments by setting up autopay on every account.

- Find your “why.” Write it at the top of your planner. Vacation fund? Home down payment? Financial security for your kids? Keep that goal visible.

- Use windfalls strategically. Tax refunds, bonuses, birthday money — put a portion directly toward debt #1. Even one lump-sum payment can shave months off your timeline.

- Stop adding new debt. While you’re paying off debt, avoid using credit cards unless you pay the balance in full each month.

- Track your net worth, not just debt. As your debts shrink, your net worth grows. Watching that number move in a positive direction is powerfully motivating.

- Pair your debt planner with a budget planner printable. Knowing exactly where every dollar goes each month means you’ll always find extra cash to throw at your debt.

You’re Closer Than You Think

Debt feels permanent — until one day, it isn’t.

The people who pay off their debt aren’t the ones with the highest salaries or the most financial knowledge. They’re the ones with a plan and the consistency to follow it month after month.

A debt payoff planner printable gives you both the plan and the structure. It removes the guesswork, keeps you accountable, and turns a mountain of debt into a manageable checklist you chip away at every single month.

You don’t need to be perfect. You just need to start.

Download your free debt payoff planner printable here, and take the first real step toward a debt-free life.

Frequently Asked Questions (FAQ)

Q: What is a debt payoff planner printable? A: A debt payoff planner printable is a worksheet you print (or use digitally) to list all your debts, organize them by payoff priority, track monthly payments, and monitor your progress toward becoming debt-free. It works as a visual roadmap for your debt elimination journey.

Q: What’s the difference between the debt snowball and debt avalanche methods? A: The debt snowball method focuses on paying off your smallest debt first for quick motivational wins, then rolling that payment into the next debt. The debt avalanche method targets your highest-interest debt first to minimize total interest paid. Both work — the best method is the one you’ll actually stick with.

Q: How do I use a debt tracker template? A: Start by listing every debt you have with its balance, interest rate, and minimum payment. Choose your payoff strategy (snowball or avalanche), then reorder your debts accordingly. Each month, make minimum payments on all debts and put any extra money toward your priority debt. Update the tracker monthly to log your progress.

Q: Can I use a debt payoff planner printable alongside a budget planner? A: Absolutely — and you should. A budget planner printable helps you identify exactly how much extra money you can allocate toward debt each month. Together, they form a complete financial management system. GuidedPlanners.com offers both in a single downloadable bundle.

Q: Is a debt payoff planner printable really free? A: Yes! GuidedPlanners.com offers a free debt payoff planner printable bundle that includes a debt snowball tracker, debt avalanche worksheet, monthly budget planner, and debt tracker template. Download instantly — no subscription required.

Published by GuidedPlanners.com — Your home for printable planners, budgeting tools, and productivity resources.