Family financial planning is the single most important thing most families never do properly.

Not because they don’t care. Because nobody ever told them how.

Most families operate on vibes. Money comes in, money goes out, and somewhere in between there’s stress, arguments, and a vague hope that things will work out.

They won’t — unless you make them.

I’ve spent years working with families, professionals, and individuals on how to get organized, build systems, and actually move toward the financial goals that matter. And what I’ve learned is this:

The gap between struggling families and thriving families isn’t income. It’s systems.

Families that win financially have a plan. They track their numbers. They set goals and review them. They know where their money is going before the month starts.

This guide gives you the full picture — from building a family budget for the first time, to managing debt, to saving for your kids’ education, to investing for retirement. No fluff. Just what actually works.

Let’s build your family financial roadmap from the ground up.

Why Family Financial Planning Matters More Than You Think

Here’s a statistic that should bother you:

The average American family carries over $10,000 in credit card debt and has less than three months of expenses saved.

That’s not a money problem. That’s a planning problem.

When you don’t have a family financial plan, every unexpected expense becomes a crisis. The car breaks down and you put it on a card. Medical bills pile up. The kids need school supplies and suddenly you’re stressed at a Target checkout.

A solid family financial planning system doesn’t just prevent those moments. It rewires how your whole family thinks about money.

What a real financial plan actually does for your family:

- Reduces money fights — because everyone knows the plan and agrees on the goals

- Builds financial security — through an emergency fund, insurance coverage, and savings habits

- Speeds up wealth building — because your money is directed intentionally, not spent reactively

- Teaches your kids — budgeting with kids involved builds financial literacy early, which is one of the greatest gifts you can give them

- Reduces stress — knowing your numbers removes the anxiety that comes from financial fog

I’ve worked with parents who felt completely buried by debt and overwhelmed by their monthly expenses. Once they had a family financial goals framework in place — something they could actually look at and work from every week — everything changed. Not overnight. But consistently.

That’s what this guide is going to help you build.

Step 1: Get Clear on Your Family’s Financial Picture

Before you can plan anything, you need to know what you’re working with.

Most people skip this step because it feels uncomfortable. Looking at your real numbers — all of them — can be confronting. Do it anyway.

Calculate Your Household Income

Add up every dollar coming into your household each month.

- Primary job salary (after taxes)

- Partner’s income

- Freelance or side income

- Child support or alimony received

- Rental income or passive income

- Any government benefits or assistance

Write that number down. That is your monthly household income. Everything else gets built around it.

List Every Monthly Expense

This is where most people get humbled.

Pull three months of bank statements and credit card statements. Go line by line. Categorize everything.

Fixed monthly expenses (same every month):

- Mortgage or rent

- Car payments

- Insurance premiums — health, auto, life, homeowner’s

- Loan payments

- Subscriptions and memberships

Variable monthly expenses (change each month):

- Groceries and household supplies

- Gas and transportation

- Dining out and entertainment

- Clothing and personal care

- Kids’ activities and school expenses

- Medical and pharmacy

Once you see the full picture of your monthly expenses vs. your income, you know exactly what you have to work with.

If the number is tight — that’s information. If you’re spending more than you earn — that’s urgent.

Either way, now you can make real decisions.

To make tracking your numbers easier, visit the Guided Planners shop for budget planners, expense trackers, and financial planning tools built specifically for families.

Step 2: Build a Family Budget That Actually Works

Budgeting gets a bad reputation because most people set unrealistic budgets and quit when they fail.

A good family budget isn’t a punishment. It’s a spending plan. You decide where the money goes before the month starts instead of wondering where it went after.

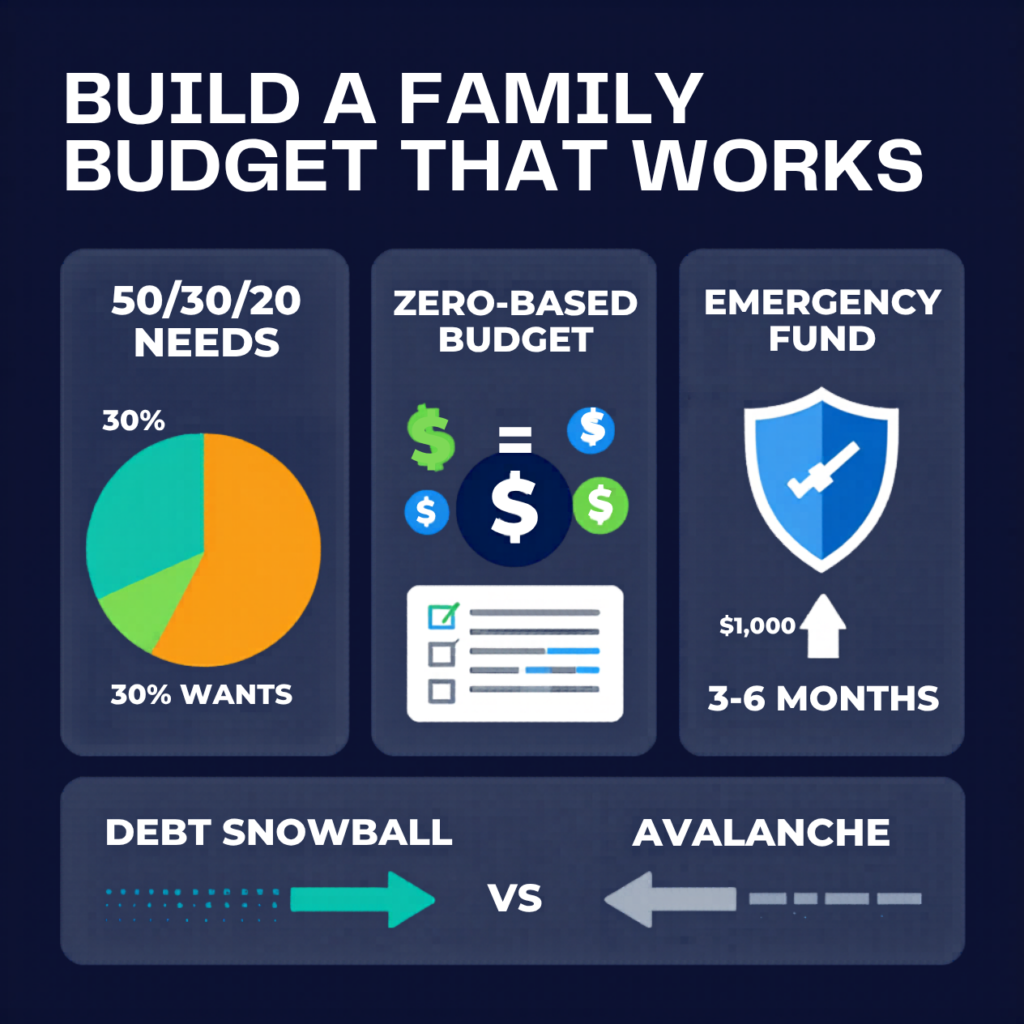

The Zero-Based Budgeting Method

Zero-based budgeting is one of the most powerful family budgeting strategies out there, popularized by Dave Ramsey and backed by strong financial research.

The concept: every dollar of income gets assigned a job before the month begins. Income minus all assigned spending equals zero.

That doesn’t mean you spend everything. It means every dollar is allocated — to expenses, savings, debt payoff, investments, or a spending category.

How to set up zero-based budgeting for your family:

- Start with your total monthly income

- List all fixed expenses first — these come off the top

- Assign amounts to variable categories based on real past spending, not wishful thinking

- Fund your savings goals and debt payoff next (more on that shortly)

- Distribute the remaining money to discretionary categories

- Confirm that income minus all assigned amounts equals zero

The first month is always messy. That’s okay. You’re building a system, not chasing perfection.

Tools like YNAB (You Need A Budget) and Mint can help you track this digitally. For families who prefer to plan on paper, our free planners collection has budget planner printables and family expense trackers you can download immediately.

The 50/30/20 Rule for Families

If zero-based feels like too much structure to start, try the 50/30/20 rule as a simple framework:

- 50% needs — housing, food, utilities, insurance, minimum debt payments

- 30% wants — dining out, entertainment, vacations, fun money

- 20% savings and debt — emergency fund, retirement accounts, extra debt payoff, college savings

This isn’t perfect for every family — especially large families or families in high cost-of-living areas. But it gives you a starting benchmark.

If your needs are eating 70% of your income, that’s the problem to solve. You either need to increase household income or reduce fixed costs.

Step 3: Build Your Emergency Fund First

Before you invest. Before you aggressively pay off debt. Before anything else — you need an emergency fund.

This is non-negotiable.

An emergency fund is the foundation of your entire family financial plan. Without it, every unexpected expense derails you. You go into debt for car repairs, medical bills, job loss. The spiral starts here.

Here’s the simple framework:

- Step 1: Build a starter emergency fund of $1,000 as fast as possible. This stops most small emergencies from becoming big ones.

- Step 2: Once high-interest debt is gone, build your

- Step 3: Keep this money in a high-yield savings account — accessible but separate from your spending account.

I worked with a family last year that had zero savings. Within eight months, they had $6,000 in an emergency fund. They did it by automating $250 per paycheck into a separate account and treating it like a bill.

They didn’t change their income. They changed their system.

That’s the power of family financial planning done right.

Step 4: Attack Debt Strategically

Debt is one of the biggest drains on family wealth. The interest you pay every month is money that could be building your future instead.

Debt management for families doesn’t have to be complicated. Two methods work best:

The Debt Snowball Method

List all debts from smallest balance to largest. Pay minimums on everything. Throw every extra dollar at the smallest balance.

When it’s gone, take that payment and add it to the next smallest.

The momentum is psychological. You get early wins. Wins build motivation. Motivation keeps you going.

The Debt Avalanche Method

List all debts from highest interest rate to lowest. Pay minimums on everything. Throw every extra dollar at the highest rate debt.

This saves the most money mathematically. But it can take longer to see your first win.

Choose the one you’ll actually stick with. The best debt payoff strategy is the one that gets finished.

Use a debt payoff worksheet — or one of the guided journals from Guided Planners — to track your progress visually. Watching the numbers go down every month is motivating in a way that no spreadsheet can replicate.

Step 5: Set and Track Family Financial Goals

Here’s what separates families that build real wealth from families that just manage to get by:

Written goals tied to specific numbers and timelines.

Vague intentions don’t work. ‘We want to save more money’ isn’t a goal. It’s a wish.

A real goal sounds like: ‘We will save $15,000 for a down payment on a house by December 2026 by putting $625 per month into a dedicated savings account.’

That’s specific. It’s measurable. It has a deadline. And you can calculate exactly what it requires.

Short-Term Family Financial Goals (Under 1 Year)

- Complete your starter emergency fund

- Pay off one credit card

- Create and stick to a family budget for 3 consecutive months

- Cut one major expense category by 20%

Medium-Term Family Financial Goals (1 to 5 Years)

- Build a full 3 to 6 month emergency fund

- Pay off all consumer debt

- Save for a home down payment

- Start a college savings plan for each child

- Build 3 months of expenses in a dedicated family savings plan

Long-Term Family Financial Goals (5+ Years)

- Reach financial independence

- Fully fund retirement accounts

- Pay off your mortgage

- Build generational wealth through investments and estate planning

- Achieve a positive net worth that grows year over year

Review your family financial goals monthly — as a couple, or as a whole family. Make it a family meeting. Show the kids the progress. This is how financial literacy gets built at home, not in a classroom.

For a structured weekly planning routine that pairs perfectly with your financial goals, our printable weekly planner for busy professionals and the weekly work schedule template help you connect daily actions to long-term financial outcomes.

Step 6: Start Investing — Even If the Amount Feels Small

People wait until they have ‘enough’ money to invest. That’s the wrong move.

Time in the market beats timing the market. Every year you wait is compound growth you’ll never get back.

Retirement Accounts First

If your employer offers a 401(k) with a match — that is a 100% instant return on your money. Start there.

After that, contribute to a Roth IRA or Traditional IRA depending on your tax situation. In 2025, the annual IRA contribution limit is $7,000 per person, $8,000 if you’re over 50.

Platforms like Vanguard, Fidelity Investments, and Charles Schwab make this straightforward and low-cost. Index funds with low expense ratios are the go-to for most families — they’re diversified, low-maintenance, and historically strong over long periods.

College Savings Plans

A 529 college savings plan (child education fund) is one of the most tax-advantaged tools available to parents.

Contributions grow tax-free when used for qualified education expenses. Many states offer additional tax deductions.

You don’t need to fund college completely. Even $50 per month started at birth compounds significantly by age 18.

The point isn’t perfection. The point is starting.

Building Passive Income

Long-term family wealth is built through passive income — money that works while you sleep.

- Dividend-paying index funds

- Rental property income

- Business ownership or side ventures

- High-yield savings and bond ladders

These don’t happen overnight. But every dollar you invest today is a future passive income stream that reduces your family’s dependence on a single paycheck.

Step 7: Protect What You’re Building

Building wealth without protecting it is like filling a bucket with a hole in it.

Insurance Planning

Insurance planning isn’t exciting. But it is essential.

- Life insurance: If anyone depends on your income, you need term life insurance. Period. A general rule is 10 to 12 times your annual income in coverage.

- Disability insurance: Most people are far more likely to become disabled than to die before retirement. Short and long-term disability coverage protects your income if you can’t work.

- Health insurance: Even with employer coverage, review your deductibles and out-of-pocket maximums annually.

- Homeowner’s or renter’s insurance: Protects your largest asset and all your belongings.

Estate Planning

Estate planning is not just for the wealthy. If you have kids, you need these documents in place:

- A will that specifies guardianship for your children

- A durable power of attorney

- A healthcare directive

- Beneficiary designations reviewed on all accounts

None of this costs much. An online legal platform can handle the basics for under $200. Not having it costs your family incalculably more.

Step 8: Improve Financial Literacy as a Family

The most overlooked part of family financial planning is education.

You can have the best plan in the world, but if your household isn’t financially literate, the plan breaks down the moment life gets complicated.

Ways to build financial literacy in your home:

- Give kids a small allowance tied to chores — and teach them to split it into spend, save, and give

- Involve your partner in all major financial decisions, not just the results

- Read one personal finance book per quarter — start with The Total Money Makeover, I Will Teach You to Be Rich, or The Millionaire Next Door

- Review your budget and progress as a couple monthly, not just when something goes wrong

- Use visual tools — budget planner printables, debt payoff trackers, savings challenges — to make abstract numbers concrete

Financial stress is the number one driver of relationship conflict. Financial literacy is the antidote.

When both partners understand the plan, agree on the goals, and track progress together, money becomes something you do together — not something that happens to you.

Family Financial Planning Checklist

Use this as your starting framework:

Month 1:

- Calculate total household income

- List all monthly expenses

- Set up a zero-based or 50/30/20 budget

- Open a separate emergency fund account

- Start contributing $250+ per month toward emergency savings

Months 2 to 3:

- Hit your $1,000 starter emergency fund

- List all debts and choose your payoff method

- Review all insurance coverage

- Write down three family financial goals with specific numbers and deadlines

Months 4 to 6:

- Start contributing to a retirement account if not already

- Research 529 plans if you have children

- Review and update beneficiaries on all accounts

- Complete or update will and estate documents

Ongoing:

- Monthly budget review with your partner

- Quarterly financial goals check-in

- Annual insurance and estate plan review

- Tax planning review in Q4

- Annual net worth calculation

Frequently Asked Questions About Family Financial Planning

How do I start family financial planning with no savings?

Start with one thing: your emergency fund. Open a separate savings account today and set up a $25 or $50 automatic transfer with every paycheck. That’s it. Don’t wait until you feel ready. Start with what you have and build from there.

What is the best budgeting strategy for a large family?

For larger families with tighter budgets, zero-based budgeting works very well because every dollar has a purpose. Combining budgeting with meal planning can also significantly reduce grocery expenses.

Should couples combine finances or keep them separate?

Many financial experts recommend shared financial planning because it improves transparency and long-term wealth building. Some couples use shared accounts for bills and savings while maintaining separate personal spending accounts.

How much should a family save each month?

A common recommendation is the 50/30/20 rule, where 20% of income goes toward savings. However, saving any consistent amount is better than not saving at all.

When should families start saving for college?

Families should begin saving for college as early as possible to benefit from long-term compound growth. Even small monthly contributions can grow substantially over time.

What tools can help with family financial planning?

Budgeting apps, investment platforms, expense trackers, printable planners, and guided financial journals can help families organize finances and track goals more effectively.

Is financial planning different for single parents?

Yes. Single parents often need stronger emergency savings, detailed budgeting, and insurance protection because they manage household finances independently.

How do I start family financial planning with no savings?

Start with one thing: your emergency fund. Open a separate savings account today and set up a $25 or $50 automatic transfer with every paycheck. That’s it. Don’t wait until you feel ready. Start with what you have and build from there.

What is the best budgeting strategy for a large family?

For larger families with tighter margins, zero-based budgeting tends to work best because it forces intentional allocation of every dollar. Pair it with a meal planning routine to cut grocery costs — often the largest variable expense for big families.

Should couples combine finances or keep them separate?

The research is clear: couples who combine finances and plan together build more wealth than those who operate separately. That said, how you structure accounts can vary. Many couples use a combined household account for shared expenses and savings, plus individual accounts for personal spending. What matters most is that both people understand the full picture.

How much should a family save each month?

The 20% rule from the 50/30/20 budget is a good starting target. But even 5% or 10% is better than zero. The goal is to start, build the habit, and increase as your income grows or debts get paid off.

When should families start saving for college?

As early as possible. Time is your biggest advantage when it comes to a college savings plan. Opening a 529 account with even $50 per month when a child is born gives you 18 years of compound growth. Starting when your child is 15 gives you three years. The difference is enormous.

What tools can help with family financial planning?

Digital tools like YNAB and Mint help with real-time tracking. Vanguard, Fidelity, and Charles Schwab are the go-to platforms for investing. For families who prefer physical planning tools — budget planner printables, expense trackers, and guided journals Guided Planners offers a full range of planners designed specifically for busy families and professionals.

Is financial planning different for single parents?

Yes — the stakes are higher. Single parents are managing household income and expenses with no backup. That makes the emergency fund even more non-negotiable, and life insurance even more essential. The structure of the plan is the same, but the urgency of protecting it is greater.

Your Family’s Financial Future Starts With a Decision, Not a Dollar Amount

I want to be direct with you about something:

You don’t need more money to start family financial planning. You need a decision.

The decision to look at your numbers honestly.

The decision to build a budget and actually follow it.

The decision to protect your family, pay off your debt, and start building something that compounds over time.

Most families overcomplicate this. They think they need a financial advisor, a certain income, or a perfect moment to start.

They don’t.

They need a plan, a budget planner, and the willingness to review it every month.

That’s it.

The wealthiest families I know didn’t get there by earning the most money. They got there by managing what they had better than everyone around them.

Better cash flow management. Better habit formation. Better goal clarity. Better systems.

You can build that. Starting right now.

Head to the Guided Planners shop and grab a planner that fits where you are right now — whether that’s your first family budget, a debt payoff tracker, a savings challenge, or a full annual budget planner. Everything you need to get organized and stay organized is there.

Family financial planning isn’t a one-time event. It’s a practice. And the families who make it a regular practice are the ones who build real, lasting financial security.

Start your practice today.

Recommended Planners & Journals to Support Your Financial Goals

Creating a strong family financial plan is much easier when you have the right tools to stay organized, track progress, and build consistent habits. Whether you’re managing a household budget, setting financial goals, tracking expenses, or improving productivity, the following planners and journals can help you stay on track:

Daily & Weekly Planner for Busy Moms

Designed for mothers balancing family responsibilities, finances, schedules, and personal goals. This planner helps you organize tasks, manage time effectively, and create a more structured household routine.

Budgeting & Expense Tracking for Home Projects

Planning a renovation, remodeling project, or major home upgrade? This planner helps you track project expenses, stay within budget, and avoid costly surprises.

Habit Tracker Journal Planner

Financial success often comes down to consistent habits. This planner helps you build daily, weekly, and monthly routines that support savings goals, budgeting discipline, productivity, and personal growth.

Home Moving Planner Checklist

Moving can be one of the most expensive life events. This planner helps you organize your move, track expenses, manage supplies, and stay financially prepared throughout the process.

The Burnout Recovery Planner

Financial stress often affects mental health. This guided journal combines daily check-ins, self-care planning, stress management tools, and therapy-inspired worksheets to help you maintain emotional well-being while pursuing your financial goals.

First-Time Homeowner Planner

Buying a home is a major financial milestone. This planner helps first-time homeowners stay organized with budgeting, maintenance schedules, important documents, and homeownership planning.

Mother of the Bride Organizer & Planner

For families planning a wedding, staying organized is essential. This planner helps manage schedules, budgets, vendor information, checklists, and important event details.

Wedding Planner Book & Organizer for Bride and Groom

A complete wedding planning solution designed to help couples organize budgets, guest lists, timelines, vendors, and wedding expenses from start to finish.

No matter where you are in your financial journey, having a structured planning system can make it easier to manage money, stay organized, reduce stress, and achieve your family’s long-term goals.

Guided Planners | Planner Design Expert | 5+ Years Designing Productivity & Financial Planning Tools for Families, Professionals, Educators & Nurses